2026年ASIC晶片雙雄:Google與Amazon在AI投資策略與北美資料中心擴張

發佈日期

2025-12-09

更新頻率

不定期

報告格式

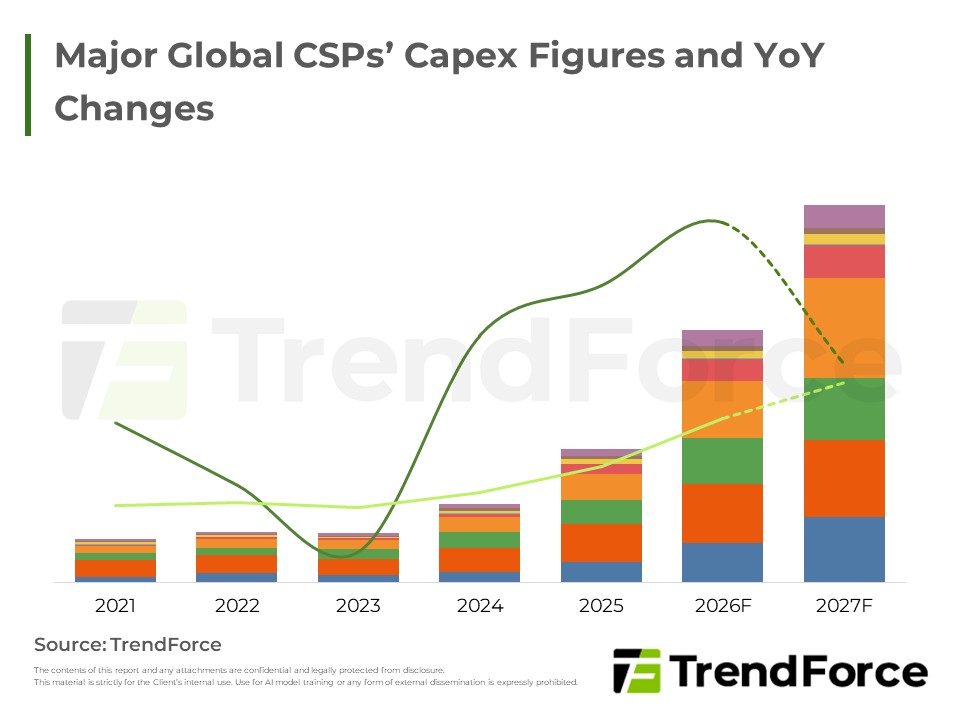

Google與Amazon憑藉自研晶片優勢,在AI算力成本效益上領先同業。Google採短期高強度建置策略以消化積壓訂單;Amazon則依靠零售現金流支撐極高的AI資本密集度,構築資料中心霸權。兩者皆致力於將技術優勢轉化為實體壁壘。

重點摘要

- 自研晶片優勢:Google與Amazon皆利用自研晶片,展現優於同業的算力成本效益與折舊承受力。

- Google全棧式擴張:策略轉向全棧式進攻,透過擴大單點規模與建設超大型園區,解決產能追趕期的龐大需求。

- Amazon交叉補貼戰略:以零售帝國的現金流交叉補貼極高的AI資本支出,在維吉尼亞州等地建立高密度的資料中心霸權。

- 關鍵競爭要素:未來的勝負關鍵在於誰能有效駕馭大規模能源吞吐與鉅額資本循環。

目錄

- 前言

- Google is Relatively Scattered in Deployment while Amazon Focuses on Northeast Region

- 1,550億積壓訂單的底氣,解讀Google AI資本密集度飆升下的護城河

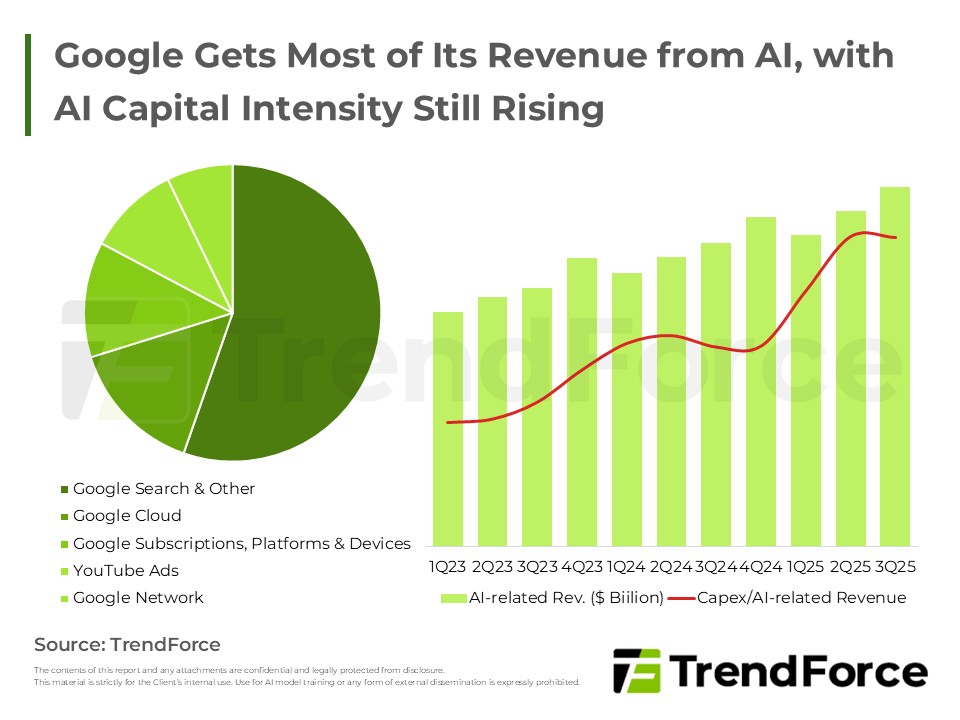

- Google Gets Most of Its Revenue from AI, with AI Capital Intensity Still Rising

- Google Broke Away from Convention by Announcing US$40 Billion of Investment in Texas

- 零售霸主的豪賭:解讀 Amazon 高 AI 資本密集度背後的雙面賽局

- Only a Small Portion of Amazon’s Revenue Is AI-Related, Yet Its AI Capex Intensity Remains Extremely High

- Amazon's Long-Term Footprint in Virginia Gives It the Highest Data Center Density in North America Among the Four Major CSPs

<報告頁數:8>

報告分類: AI/HBM/Server